|

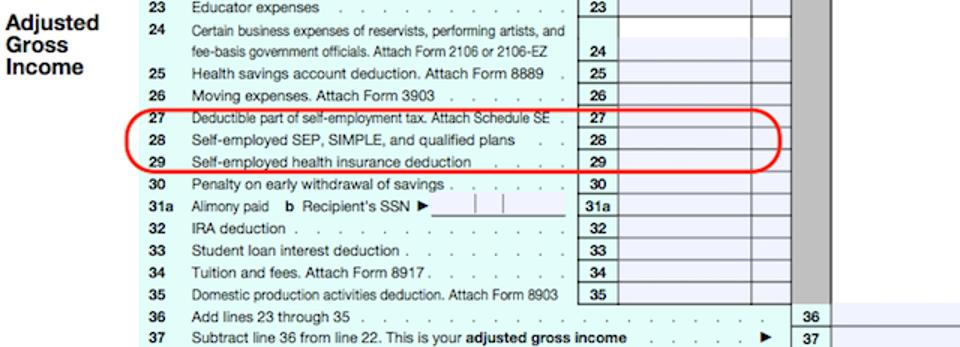

By Kelly Phillips Erb  "American business is overwhelmingly small business." That's the word from the Small Business & Entrepreneurial Council which cfigured that the number of small businesses with fewer than 20 workers together with the number of nonemployer businesses makes up 97.9% of the businesses in America (remember those are numbers of businesses and not numbers of employees). Data from the Internal Revenue Service (IRS) supports the notion that small businesses are making a significant economic impact. Of the nearly 148 individual income tax returns filed in 2014 (the last year for which complete data is available, downloads as a pdf), 46 million - or 1/3 - of tax returns reported income from a sole proprietorship, pass-through business entity (like an s corporation, partnership or LLC), rents/royalties, or farms. That's 1 in 3 individual taxpayers who filed an individual tax return reporting business-related income. It's no wonder that a number of the questions in our last #AskForbes Twitter chat focused on deductions for small business. To help you out, here are 10 can't miss tax breaks for small businesses and self-employed persons: 1. Self-employment tax. You already know that wages are subject to Social Security and Medicare taxes, together called FICA (Federal Insurance Contributions Act) taxes or payroll taxes since they are taken right out of your paycheck. Not everyone is aware, however, that there are corresponding taxes on self-employment income, sometimes called SECA (Self-Employment Contributions Act). A key difference between the two is that if you are employed by a business, you pay Social Security (6.2%) and Medicare tax (1.45%) as the employee, and your employer kicks in tax at the same rates (6.2% and 1.45%, respectfully) on your total wages. If you’re self-employed, you pay both portions. Fortunately, you can deduct the portion of your self-employment tax equivalent to what an employer would pay (meaning Social Security (6.2%) and Medicare tax (1.45%)) on the front page of your tax return on line 27 (highlighted below) as an "above-the-line" deduction, or adjustment to income. You can't deduct the other portion of Social Security and Medicare taxes but hey, neither can wage earners. (For more on how Social Security wage tax numbers bumped up, resulting in a higher tax bill this year, see this prior post.) 2. Retirement savings. If you contributed to a self-employment SEP (simplified employee pension) plan, SIMPLE (savings incentive match plan for employees) plan, or qualified plan like an H.R. 10 or Keogh plan during the year, you can deduct contributions you make to the plan for yourself on the front page of your tax return on line 28 (highlighted below). Small business owners get a break, too: you can deduct contributions you make to a retirement plan for your employees (sole proprietors would deduct those on Schedule C or Schedule F while partnerships and corporations would deduct them on their entity's tax form). You can also deduct trustees' fees if contributions to the plan don't cover them. All kinds of rules and limits apply to retirement plans, so I suggest that you work with a plan administrator or financial advisor. (For more on small business retirement plans, click here.)  3. Self-employed health insurance deduction (& other medical expenses). Health insurance is one of the most expensive purchases you may make all year for your business. Fortunately, you may be able to deduct the amount you paid for health insurance, including Medicare premiums you voluntarily pay, for yourself, your spouse, and your dependents (including your child under age 27 at the end of 2016). To qualify for the self-employed health insurance deduction, you must have a net profit for the year reported on Schedule C, Schedule C-EZ, or Schedule F, and the insurance plan must be established, or considered to be established, under your business. If you qualify, you'll deduct the cost of the premiums on the front page of your tax return on line 29 (highlighted above). As with retirement savings, if you have employees, you can deduct the cost you pay for a corresponding plan (sole proprietors would deduct those on Schedule C or Schedule F while partnerships and corporations would deduct them on their entity's tax form).

Claiming the self-employed health insurance deduction doesn't bar you from deducting other medical expenses: if you itemize, you can still include your out-of-pocket medical expenses, like doctor's visits and prescriptions, on a Schedule A (with the exception of your health care premiums, obviously). (Maneuvering the ever-changing health care system can be tricky: I strongly suggest that you work with a qualified broker. For more on paying for health care as a small business, click here.) 4. Advertising & promotion costs. You're allowed a deduction for the costs associated with getting the word out about your business. This can include not only obvious advertising like Yellow Pages or newspaper, magazine, TV or radio advertising but also less in-your-face promotions like the cost of printing business cards and business related swag. And it's not just the final product that's deductible: you can also deduct reasonable costs of coming up with ad copy or slogans, as well as creating graphics and logos. The costs associated with your website are deductible, including the cost to purchase and maintain the site and hosting fees. Think outside of the box, too: the costs of creating and hosting seminars and workshops meant to lure in customers can be deductible as are community sponsorships, like putting your business name on Little League and other team tee-shirts. 5. Car & truck-related expenses. You can deduct the cost of expenses related to a car or truck, including lease payments, so long as you use your vehicle exclusively for business. If you split the use of the vehicle for personal and business purposes, you can only deduct the portion attributable to business (this, of course, means you need to keep good records, such as a mileage log, showing when you use the vehicle for business). To calculate your deduction, you can use the standard mileage rates (you'll multiply the rate by your business mileage and add that amount to your expenses for parking fees and tolls), or you can deduct the actual expenses (such as gas, oil, repairs, insurance, and license plates). Limits and other rules may apply so check with your tax professional for details. (For 2016 standard mileage rates, click here. For 2017 standard mileage rates, click here.) 6. Insurance premiums. You can typically deduct premiums that you pay for business related insurance. This can include errors and omissions insurance; professional malpractice insurance; general liability insurance; and workers compensation insurance, as well as the cost to insure your premises from fire, storm, theft, accident, or similar losses (but see #8 below - and remember that health care insurance is deducted separately). Source:http://www.forbes.com/sites/kellyphillipserb/2017/02/13/10-cant-miss-tax-deductions-for-small-businesses-self-employed-persons/#4a83a45051d9 |

Marcus Guiliano

Catch up on my current posts along with industry articles Archives

March 2020

Categories |

RSS Feed

RSS Feed

Marcus Guiliano Productions LTD

PO Box 731

Ellenville NY 12428

(845) 647-3000

www.MarcusGuiliano.com

Disclaimer

This site is not a part of the Facebook website or Facebook Inc. Additionally, This site is

NOT endorsed by Facebook in any way. FACEBOOK is a trademark of FACEBOOK, Inc.

DISCLAIMER: The sales figures stated above are my personal sales figures. Please understand my results are not typical, I’m not implying you’ll duplicate them (or do anything for that matter). I have the benefit of practicing direct response marketing and advertising since 2009, and have an established following as a result. The average person who buys any "how to" information gets little to no results. I’m using these references for example purposes only. Your results will vary and depend on many factors …including but not limited to your background, experience, and work ethic. All business entails risk as well as massive and consistent effort and action. If you're not willing to accept that, please DO NOT GET OUR INFORMATION.

This site is not a part of the Facebook website or Facebook Inc. Additionally, This site is

NOT endorsed by Facebook in any way. FACEBOOK is a trademark of FACEBOOK, Inc.

DISCLAIMER: The sales figures stated above are my personal sales figures. Please understand my results are not typical, I’m not implying you’ll duplicate them (or do anything for that matter). I have the benefit of practicing direct response marketing and advertising since 2009, and have an established following as a result. The average person who buys any "how to" information gets little to no results. I’m using these references for example purposes only. Your results will vary and depend on many factors …including but not limited to your background, experience, and work ethic. All business entails risk as well as massive and consistent effort and action. If you're not willing to accept that, please DO NOT GET OUR INFORMATION.